Recent weeks brought severe price shocks in many markets. Their timing and severity took most participants by surprise. In these circumstances, I-System strategies performed superbly well. As this post shows, a few strategies sustained negative results, but this is to be expected. This is why, rather than formulating a trading strategy, we built a stable knowledge framework so that we can formulate and implement literally thousands of strategies within that framework. In this sense I-System holds potential to entirely transcend uncertainty by supplanting it with a more predictable risk class: a swarm of consistent, intelligent and emotionless trading agents, each in charge of a small fraction of portfolio risk. The current experience was an important test for the I-System. The results speak for themselves. Continue reading

Category Archives: Oil market

Market panics and trend following

Today global capital markets opened to unprecedented price dislocations. ZeroHedge captured the mood: “Panic Purgatory: Oil Crashes to $27%; S&P Futures Locked limit Down, Treasuries Soar Limit Up Amid Historic Liquidation.” Over the recent months I’ve posted many articles on this blog and on SeekingAlpha, basically along two themes:

1) Warning that the markets would experience great turbulence in the near future (see here: “Perfect Storm Gathering…” and

2) Suggesting that the best way to navigate through the storm is by using high-quality systematic trend following strategies (see here, “Trend Following Might Save Your Tail“).

It may be that the time of reckoning has begun But if you followed my advice and used systematic trend following, most likely you’d be having a good day today. The chart below illustrates the net positioning of my 493 I-System strategies at market open this morning: Continue reading

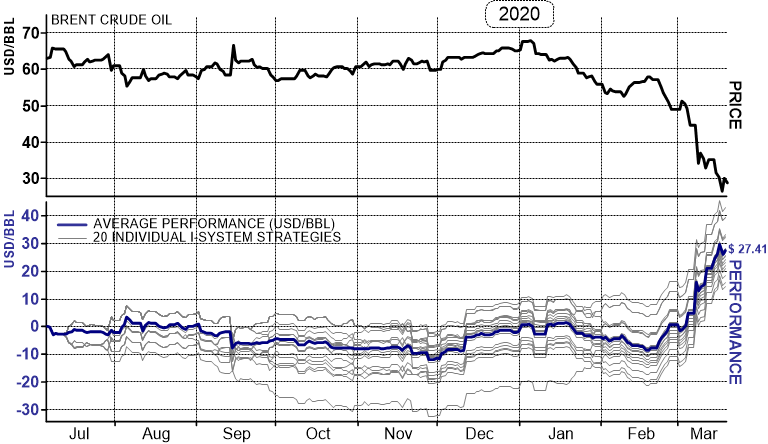

In October 2019 I predicted the current oil price collapse. How I knew? Here’s how:

In January last year, Reuters polled 1,000 oil market experts who basically agreed that oil would remain anchored in the $65-$70/bbl range through 2023. Only 3% of these experts thought that oil might rise to $90/bbl or more in 2020. I posted my analysis at this link: Market Fundamentals and Forecasting Groupthink. Later that year I published my own analysis, “Next Move in Oil Prices: $5-$10 Lower,” concluding that, …oil price will likely see another leg down… with Brent falling toward high $40s and WTI toward low $40s. Continue reading

Perfect storm gathering: the three converging disruptions

In the near future, we are likely to experience severe consequences of three converging disruptions:

- Stock market crash

- Oil price shock

- Inflation

Since the last recession we’ve enjoyed the longest ever period of economic expansion with low interest rates, low inflation and subdued commodity prices. But this all could be coming to an end.

Bursting of the “everything bubble”

Throughout the west, unprecedented government and central bank stimulus programs helped inflate the current “everything bubble.” This is not a new phenomenon; monetary expansion always creates asset bubbles. The one thing we know is that without exception, asset bubbles ultimately burst. The examples are many and some of them made a mark in the collective conscious of entire generations, from the 1630s Tulip Mania to the 1990s dot-com bubble. Continue reading

Trend following and the impact of unforeseen events

“Yes, but how can your system know if XYZ happens and markets go haywire?” This is one of the two most frequently asked questions about systematic trading strategies I’ve used over the last 20 years. Most traders tend to rely on analyses of supply and demand fundamentals to form a judgment about future price changes.

My contention is that this simply does not work and I can make a strong case to back this up (see here, here or here). I can also offer evidence that my systematic approach does work (see here or here) even if I know nothing about the supply and demand economics of most markets I cover. This usually elicits the objection that my system can’t know if some XYZ event might happen tomorrow (recently, XYZ tended to refer to Trump tweets), upsetting the markets and rendering my strategies ineffective. Recent experience afforded me an (almost) perfect answer to this question (plus another important issue related to trend following). Continue reading

More bad news from Saudi Arabia

Over the years I’d highlighted the increasingly dubious status of Saudi Arabia as the world’s oil production powerhouse. This year we learned that their flagship oil field Ghawar produced much less than everyone knew, now courtesy of Bloomberg we find another disconcerting bit of information corroborating these doubts as the following chart illustrates:

There can be little doubt that we are facing a grave and serious energy predicament going forward. Our economies and societies better begin preparing yesterday. Links to my research outlining the fundamental supply and demand conditions can be found here: Continue reading

The oil price shock: has it arrived?

Experts seldom expect surprises. In spite of the ever deepening economic and political uncertainties gripping most oil producing and oil consuming regions, most market experts surveyed last year predicted that oil price would fluctuate between $65 and $70 through 2023.

That forecast assumes that nothing unforeseen would happen over the next five years. Such an assumption, to put it politely, is unjustified and the list of reasons is long and complex, and it can be neither ignored nor wished away. Over the recent months I’d written a handful of articles on the subject of the ‘coming oil price shock.’ Here are the last three: Continue reading

Failure of price forecasting: the unit of account conundrum

In addition to the better understood challenges of market analysis, like access to timely and accurate data, there is another – rather massive, but usually completely ignored – problem that renders forecasting largely an exercise in futility.

Over the years I’ve written quite a bit on the unreliable nature of price forecasts based on the analysis of market supply and demand . Most recently, in “Market fundamentals, forecasting and the groupthink effect,” I discussed the problem of data quality as well as the very real problem of groupthink among leading analysts, providing an example of a staggeringly wrong oil price forecast they produced. Some of the very same experts later produced this gem: Continue reading

Market fundamentals, forecasting and the groupthink effect

Last month I had the privilege of meeting with Jaran Rystad of Rystad Energy to discuss strategic cooperation between our companies. On the occasion, he gave me a rather detailed presentation of his firm’s energy intelligence database. I must say, in my 20+ years trading in commodities markets this is by far the most impressive product of its kind I’ve ever seen. Even from the software engineering point of view, I was very impressed. For full disclosure, nobody asked nor encouraged me to write this. Much as you’d recommend a restaurant where you ate well or a doctor you respect, I wholeheartedly recommend Rystad Energy as a provider of energy market intelligence as a matter of giving credit where credit is due.

Monaco, June 2019 – with Jarand Rystad

However, even with top notch data on economic supply and demand fundamentals, divining the future remains difficult and unlikely. John von Neumann rightly said that forecasting was “the most complex, interactive, and highly nonlinear problem that had ever been conceived of.” Continue reading

The coming oil price shock 3: saber rattling in the persian gulf

- Trump Administration put their credibility on the line by taking a hard line on Iranian oil exports, pledging to collapse them to zero.

- Iranian officials matched the rhetoric by promising to close the Straits of Hormuz entirely to oil traffic. A third of world’s traded oil production transit through that choke-point.

- Assurances of ramped-up oil production from Saudi Arabia and Opec appear as firm as a wet noodle.

U.S. taking a hard line on Iran oil exports

Over the Easter weekend we’ve seen an escalation of Trump Administration’s rhetoric toward Iran. On Monday, 22 April, State Secretary Pompeo issued an official statement pledging that after their expiry on May 2, the U.S. would not renew any of the waivers enabling Iran to export crude oil. Iran’s oil exports have already dwindled from 2.5 million barrels per day last April to around 1 million barrels, and the official U.S. policy is to bring Iranian oil exports to zero.

In taking the hard line against Iran, the Trump administration has put its credibility on the line. Secretary Pompeo followed up the official announcement on twitter, stating that, “maximum pressure” means maximum pressure. Trump backed him up promising “full sanctions…”