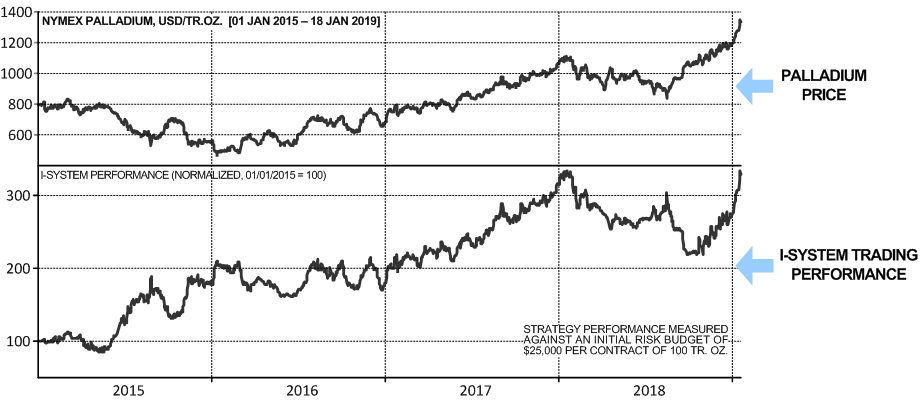

Palladium price has more than doubled since the early 2016 making the white metal more valuable than gold for the first time since 2002. Its impressive performance attracted much attention from the financial press, which published numerous articles and analyses about the palladium market. If you diligently read the analyses, you may learn that automotive industry accounts for some 75% of demand for palladium, that its global production is as little as about 200 metric tons per year (vs. about 3,000 tons for gold), that only two countries (Russia and South Africa) produce more than three quarters of its global supply, and that the demand for palladium is expected to continue to grow. Presumably that implies that palladium price should remain high and possibly continue to rise. Continue reading

Tag Archives: Markets

Parabolic markets may signify onset of high inflation

Asset price inflation might signal debasement of the currency and acceleration of commodity price inflation

This time it may well be different… For several years now, numerous high-profile commentators and analysts have been forecasting an imminent stock market correction, or indeed a crash, evoking the events of 1929, 1987, 2000 or 2008. Of course, many are now predicting it is sure to happen in 2018. If not, perhaps in 2019 or maybe 2020? Who knows… But so far, not many analysts – if any, apart from yours truly – have considered the possibility that this rally might extend even higher from today’s dizzying heights. In an October 2016 post I suggested that this is exactly what was ahead. Continue reading

The illusion of expertise in financial markets

Participants in financial markets have to deal with uncertainty on a daily basis. Their need to research and understand markets has given rise to a massive industry delivering security prices, reports and expert analyses to traders and investors seeking to make sense of the markets and predict how they might unfold in the future.

The need to understand stuff is innate to our psychology: when something happens, we almost reflexively want to know why it happened. But the compulsion to pair an effect with its cause sometimes gets us jumping to conclusions. If such conclusions turn out to be mistaken or irrelevant, they could prove useless – or something worse. Consider two recent titles from the ZeroHedge blog, published 89 minutes apart: Continue reading

The crucial importance of trends

In Berkshire Hathaway annual report (1985), Warren Buffett wrote the following:

When a management with reputation for brilliance tackles a business with reputation for poor fundamental economics, it is the reputation of the business that stays intact. [1]

My wife and I recently spent some time in Egypt. For a few days we sailed up the Nile from Luxor to Aswan on a cruise ship that counted nearly 70 crew members serving the total of five guests. The manager of the vessel was Mr. Khaled, an impeccably polite and always well dressed man in his 40s who, in spite of running a nearly empty ship managed to keep the crew’s morale high and ran the ship’s operations admirably well. Unfortunately, even if Mr. Khaled were the world’s best cruise ship manager, this particular situation was a good illustration of what Warren Buffet was talking about in his 1985 annual report. Continue reading

Why we can’t predict the behaviour of complex systems (markets, economics or climate)

Over the last century or so, science has made immense progress in understanding natural phenomena like the weather and social phenomena like markets and economics. Unfortunately, we still fall well short of being able to successfully predict their behaviour. In spite of the mindboggling leaps in knowledge and computing horsepower, systematically successful prediction continues to elude us. This is largely due to the difficulty in modelling complex systems in sufficient detail. An aspect of this problem, called “sensitive dependence on initial conditions” might well be altogether insurmountable. Continue reading