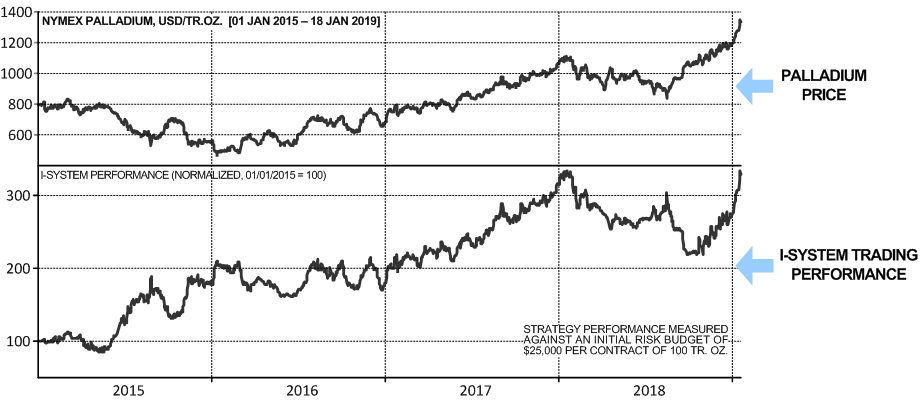

Palladium price has more than doubled since the early 2016 making the white metal more valuable than gold for the first time since 2002. Its impressive performance attracted much attention from the financial press, which published numerous articles and analyses about the palladium market. If you diligently read the analyses, you may learn that automotive industry accounts for some 75% of demand for palladium, that its global production is as little as about 200 metric tons per year (vs. about 3,000 tons for gold), that only two countries (Russia and South Africa) produce more than three quarters of its global supply, and that the demand for palladium is expected to continue to grow. Presumably that implies that palladium price should remain high and possibly continue to rise. Continue reading

Tag Archives: Commodity risk

Economic forecasting is exercise in futility

“Economists can’t forecast for a toffee… They have missed every recession in the last four decades. And it isn’t just growth that economists can’t forecast; it’s also inflation, bond yields, unemployment, stock market price targets and pretty much everything else.” – James Montier

Forecasting commodity prices and economic indicators is demonstrably an exercise in futility. Our markets and economies are complex systems and as such, their future unfolding is impossible to predict with any degree of certainty. Concretely, let’s take a look at how the leading economic analysts did at predicting oil prices, GDP growth, unemployment and stock market indices. Continue reading

Risk, Uncertainty and Profit

Frank Knight, the grand old man of Chicago wrote “Risk, Uncertainty and Profit,” one of the five most important economics books of the 20th century. Among other invaluable insights, Knight proposes that, “The responsible decisions in organized economic life are price decisions; others can be reduced to routine.” Knight recognized that price at which a firm sells its products or purchases materials tends to have greater impact on profitability than any other element. Based on the income statement of an average S&P 1500 company (and assuming constant sales volumes), a 1% improvement in the selling price would generate an 8% increase in operating profits. Conversely, a 1% drop in the cost of goods sold would lead to a 5.36% increase in operating profits. This impact was more than double that of a 1% increase in sales volume[1]. For commodity businesses where operating margins are typically very low, hedging can have a much greater impact on profitability. Continue reading