Last month I had the privilege of meeting with Jaran Rystad of Rystad Energy to discuss strategic cooperation between our companies. On the occasion, he gave me a rather detailed presentation of his firm’s energy intelligence database. I must say, in my 20+ years trading in commodities markets this is by far the most impressive product of its kind I’ve ever seen. Even from the software engineering point of view, I was very impressed. For full disclosure, nobody asked nor encouraged me to write this. Much as you’d recommend a restaurant where you ate well or a doctor you respect, I wholeheartedly recommend Rystad Energy as a provider of energy market intelligence as a matter of giving credit where credit is due.

Monaco, June 2019 – with Jarand Rystad

However, even with top notch data on economic supply and demand fundamentals, divining the future remains difficult and unlikely. John von Neumann rightly said that forecasting was “the most complex, interactive, and highly nonlinear problem that had ever been conceived of.” While the quality of data matters, the “price discovery” process involves market participants’ psychology and depends on the way we collectively perceive the market conditions, not on their objective reality. At times, perceptions veer off far from reality and prices overshoot or undershoot their “equilibrium” levels by a wide margin. They can remain there over disconcertingly long time periods. But as we’re about to see, forecasting also involves the very forecasters’ psychology.

Experts: often wrong, at times badly wrong

Every year, the U.S. Energy Information Administration (EIA), the statistical and analytical agency within the U.S. Department of Energy, publishes an exhaustive report titled International Energy Outlook that, amongst other information, provides long-term oil price forecasts. The forecasts are generated by the EIA as well as a group of the industry’s leading research institutions.

In 2003, as oil was still trading between $20 and $30 per barrel, all the submitted forecasts for 2005 were clustered between $19 and $24 per barrel. Indifferent to these authoritative predictions, crude oil continued rising with the year’s average vaulting to over $55 per barrel – 2.5 times higher than the average EIA forecast. Getting a forecast wrong is one thing. But the fact that all the forecasts were clustered so closely together points to another problem.

The groupthink effect

A “serious” research outfit stakes its reputation on forecasts they produce. In that respect, standing out from the crowd can be risky. If you get it wrong, and you’re wrong not just by a little bit, you risk your reputation, being subject to ridicule and worse. Thus, even if in 2003 some bold analyst armed with good data correctly estimated that oil prices would more than double through 2005, their firm would be unlikely to publish such a forecast. In this sense, the expert community does tend to generate something of a groupthink effect.

A recent example of this was a Reuters survey of over one thousand energy market professionals published in January this year. All these experts thought that the oil price would average between $65 and $70 a barrel through 2023. Only 3% of them expect that Brent Crude Oil might increase above $90/bbl next year. Live and see.

Overreliance on market price forecasts

But the real problem with forecasts is not that many of them turn out wrong. The problem is that far too many market professionals rely on them to make hedging and investment decisions. A large 2006 T. Rowe Price/Citigroup survey of market professionals in the financial industry revealed that well over 60 %[1] of them rely most heavily on economic forecasts for their investment decisions. This is likely to be the case in other industries as well.

Complacency can carry a devastating price tag

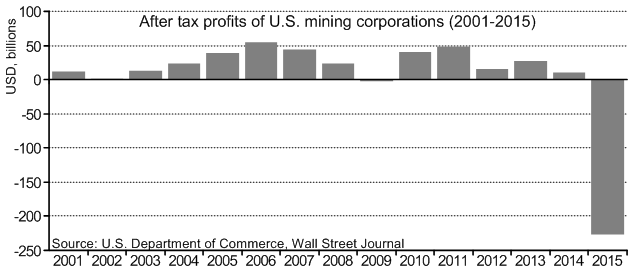

Today again, the expert groupthink on the oil price also risks misleading managers into complacency. Getting caught unprepared by unforeseen events can be devastating. How devastating? When the price of oil collapsed some 70% between the summer of 2014 and January 2016, U.S. mining industry, which includes oil and gas producers, sustained $227 billion in losses, wiping out eight previous years’ worth of profits.

Just as nobody believed in 2003 that oil prices could more than double through 2005, and rise sevenfold in the next five years, few expected that in 2015 they would collapse by 70%. But such events do happen and they are happening more often.

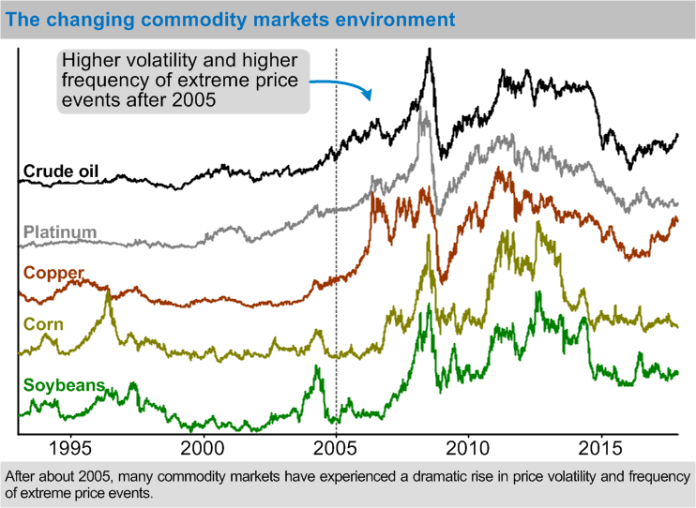

Since about 2005/6, many commodity markets have experienced a dramatic increase in volatility and frequency of extreme price events. These events represent the single greatest source of external risk for commodity firms.

Mastering the commodity price uncertainty

Given that timing and direction of extreme price events are unpredictable, how can firms master the resulting uncertainty and gain control over this source of risk? Fortunately, there’s good news hidden in the very nature of price fluctuations. Observed day-to-day, markets appear to be driven by news events and data. However, extreme price events almost invariably unfold as trends. Such trends can span many months or even years, offering us the opportunity to capture value from them.

We can capture value from price trends by using systematic trend-following strategies. Such strategies can help hedgers decide when to hedge their price exposure and when to keep it unhedged. In this way, without needing to predict the future, commodity related firms can turn price risk into a source of profits and competitive advantage.

Of course, this is all easier said than done and industry practitioners, who honed their skills in the operational aspects of their core business, tend to be reluctant to engage in price speculation. For a number of good reasons, they are right to be cautious. Nevertheless, quality solutions to this problem do exist and given the importance of price risk management, they should be explored.

At Altana Wealth, we’ve developed I-System technology. After more than 15 years of continuous use we genuinely believe it to be the Rolls Royce standard in navigating market trends. Relying on this type of systematic trend-following model, rather than on market forecasts, offers market professionals a way to navigate the commodity price roller-coasters profitably and with peace of mind. The following 12-minute video discusses our approach as well as our track record in managing price risk with I-System:

The beauty of this approach to risk management is that practitioners do not need to bet the proverbial ranch on it. They can test it on a limited portion of their risk exposure, analyse results, and expand on the concept as they acquire experience and know-how.

This year we will be rolling out a concrete service offering for industry hedgers to offer them the full benefit of our 20+ year experience managing financial risk and trading in a wide variety of commodity markets. For more information, please write to sales@altanawealth.com or contact me at alex.krainer@altanawealth.com

Alex Krainer [alex.krainer@altanawealth.com] is a hedge fund manager and commodities trader based in Monaco. He wrote the book “Mastering Uncertainty in Commodities Trading”

Notes:

[1] This 2006 survey of asset managers and pension funds from 37 countries managing some $30 trillion in assets was co-sponsored by T. Rowe Price Global Investment Services Limited and Citigroup. Questioned about what would drive their investment decisions over the next five years, majority of respondents indicated they would most heavily rely on the “medium term outlook in the bond markets,” (67%) and “global/regional economic prospects” (62%).