“Yes, but how can your system know if XYZ happens and markets go haywire?” This is one of the two most frequently asked questions about systematic trading strategies I’ve used over the last 20 years. Most traders tend to rely on analyses of supply and demand fundamentals to form a judgment about future price changes.

My contention is that this simply does not work and I can make a strong case to back this up (see here, here or here). I can also offer evidence that my systematic approach does work (see here or here) even if I know nothing about the supply and demand economics of most markets I cover. This usually elicits the objection that my system can’t know if some XYZ event might happen tomorrow (recently, XYZ tended to refer to Trump tweets), upsetting the markets and rendering my strategies ineffective. Recent experience afforded me an (almost) perfect answer to this question (plus another important issue related to trend following).

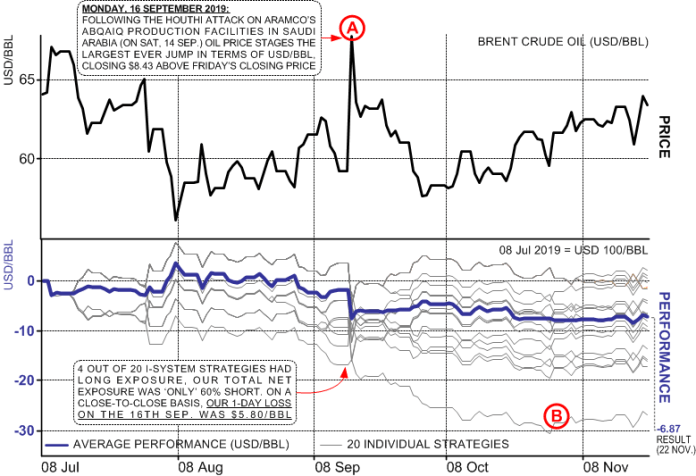

Namely, a few months ago, the manager of a well respected hedge fund asked me to put together a portfolio of strategies covering energy markets. While he’s had stellar performance over the years, even winning a number of industry awards, he’s found markets much more difficult to read in the last few years and thought he’d look into quantitative strategies. So here’s what happened – I produced this chart summarizing the results through 22 November (performance has improved since):

(A) How can the system ‘know’?

Event marked (A) answers the question about how the system can react to an unforeseen event. Military attack on Saudi oil production facilities triggered the largest ever one-day jump in oil price on 16 September 2019. Our Brent strategies had a 60% short exposure, resulting in loss that averaged $5.80/bbl for the day. This was a painful experience, but not remotely catastrophic (to trade a single contract of Brent Crude Oil, I recommend reserving a risk budget of at least $15/bbl).

The psychology of it…

But it is important to appreciate that such an experience also has a strong psychological aspect: the price spike, the losses, the thinking related to the incident and its emotional impact can easily induce traders to succumb to impulsive trading around unfolding events. This can exacerbate losses rather than mitigating them. By contrast, reliance on quality systematic decision support gives traders the grounding to keep their composure and resist getting caught up in the commotion. The inertia of systematic trading during tumultuous events need not be regarded as a weakness of the approach. To the contrary, it could be an important strength.

All in longer-term perspective

Investment trading entails risk taking, and this implies the possibility of incurring losses. That’s inevitable and an investment manager’s key responsibility is to manage the risks. As I’d written in “Six Principles To Adopting Best Practices in Commodity Price Hedging,” the proper role of risk management is to enable controlled and purposeful risk taking, to accept occasional losses and to communicate such losses to stakeholders openly and transparently, without them losing confidence in the manager’s strategic objectives or his ability to achieve them.

Over the long term, those objectives are far more likely to be achieved through disciplined adherence to a well-formulated strategy than by attempting to trade oneself out of every loss or avoiding all adverse impacts from unforeseeable events or Trump’s tweets.

(B) Some strategies will do poorly

One of our Brent strategies (marked B in the above chart) lost nearly $30/bbl over the observed four-month period. This happens: over any given time period, some strategies will turn out lousy. We can only know how a strategy did in the past. We don’t know how it might do in the future. As Danish philosopher put it, “Life can only be understood backwards; but it must be lived forwards.”

We sought to mitigate this risk by building the I-System. Rather than formulating a trading strategy, we built a knowledge framework that can track a large number of trading strategies in any market. This enables us to fragment risk among a diverse set of virtual traders. Over any time period, some of them will lag and some will excel. Using many of them greatly reduces the risk of disappointing results and improves the likelihood of satisfactory results.

In our present case, the overall performance was negative. As the above chart illustrates, our Brent strategies on average sustained a loss of $6.78/bbl. However, all but $1.07 of that was the result of the attacks in Saudi Arabia. In other words, if it weren’t for that event, we would have lost just over $1/bbl over a 4-month period. In absence of a clear market trend, this result was simply superb: without clear price trend, trend-following strategies aren’t likely to perform.

Consider for example, that managing the same exposure to oil price with options would cost at least $10/bbl in premiums (for at-the-money, 30-day call options). Using those awesome ‘structured products’ your friendly banker hawks could cost twice as much. Keep in mind that in ordinary circumstances around half of all options expire worthless. When volatility spikes, upwards of 90% of them expire worthless. In this context, I-System performance compares very favorably.

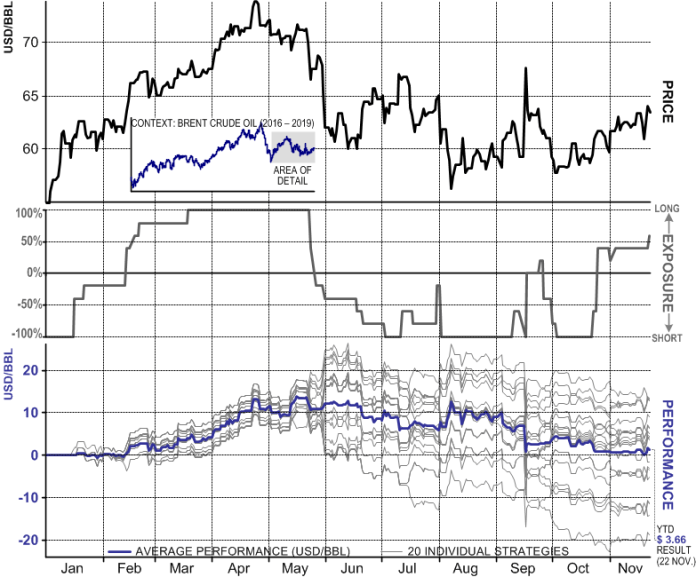

Before wrapping up, below is the chart of the same set of I-System Brent strategies from the beginning of 2019:

Almost without exceptions, when markets trend, I-System generates positive performance, as we saw in the first half of 2019 (and are seeing presently as oil price started trending higher). From there on, the question is not whether the model/strategy works or not but whether or not markets move in trends.

Alex Krainer is a commodities trader based in Monaco. He wrote the 5-star rated book “Mastering Uncertainty in Commodities Trading”