Recent weeks brought severe price shocks in many markets. Their timing and severity took most participants by surprise. In these circumstances, I-System strategies performed superbly well. As this post shows, a few strategies sustained negative results, but this is to be expected. This is why, rather than formulating a trading strategy, we built a stable knowledge framework so that we can formulate and implement literally thousands of strategies within that framework. In this sense I-System holds potential to entirely transcend uncertainty by supplanting it with a more predictable risk class: a swarm of consistent, intelligent and emotionless trading agents, each in charge of a small fraction of portfolio risk. The current experience was an important test for the I-System. The results speak for themselves.

Extreme price events are among the greatest sources of risk

For traders and investors, extreme price events represent one of the greatest sources of risk. Global markets sustained unprecedented price shocks over the last month. After peaking on the 20th February, equity indices dropped by 30% (S&P500) or more. Oil prices shed nearly 60% from their January peaks and treasury futures rallied sharply to new all-time highs. I-System strategies performed superbly well through these unforeseeable events.

Extreme price events are unpredictable

Extreme price events can’t be predicted using conventional methods of market research and systematic trend following represents the only reliable and effective method of navigating such storms reliably and effectively. Systematic trend following is a simple concept, but rather difficult to get right – we discuss this briefly with the review of our silver strategies. Below I summarize their performance in crude oil, silver and treasury futures markets.

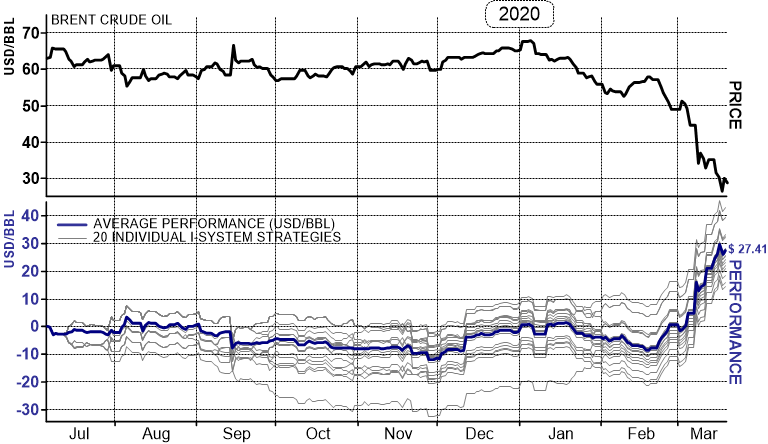

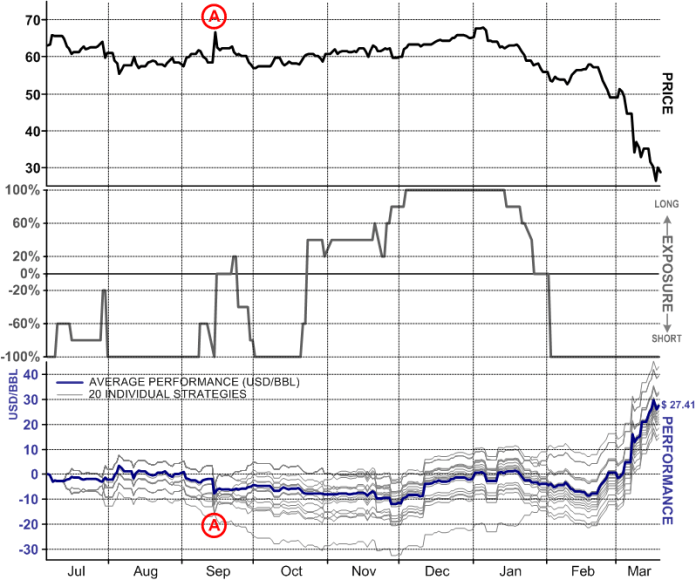

1. Brent Crude Oil

After many months of sideways action around the $60/bbl level, crude oil started trending through November and December last year. I-System strategies gradually shifted to the long side and generated moderate gains through early January. However, subsequent reversal caused more losses until the reversal turned into an accelerating down-trend. By February, all 20 strategies switched to the short side (at abt. $58/bbl on average), generating strong profits through the price collapse.

From July 2019, the strategies generated a profit of $27.41/bbl. This estimate assumes all trades executed at market open, paying $5/ commission per contract per transaction (incl. 9 roll-over trades, selling the expiring contract and buying the next delivery). Some of the strategy curves overlap so not all 20 are visible. The price spike marked (A) in the above chart represents market reaction after the 14 September incident in Saudi Arabia.

Yes but, how can your model ‘know’ if XYZ happens?

This is the most commonly voiced misgiving about quantitative strategies. Event A in the above chart – the largest recorded 1-day oil price jump – is a good case in point. On Saturday, 14 Sep. 2019, a missile attack in Saudi Arabia caused substantial damage to Aramco’s Abqaiq oil production facilities. The following Monday, oil price closed $8.42/bbl above previous Friday’s price. Of course, I-System strategies didn’t ‘know’ this would happen and held 60% short exposure at the time. As a result, the portfolio sustained a $5.80/bbl average loss (4 out of 20 strategies had long exposure). This can easily induce traders to react emotionally. But impulsive trading around on-going events can make things worse. By contrast, disciplined adherence to predefined and tested decision-making rules enable traders to resist getting caught up in the commotion of the moment. In this sense, I-System guidance is not a weakness but an important strength. Over longer time-horizons, its consistency in the face of uncertainty pays off, as Exhibit 1 clearly shows.

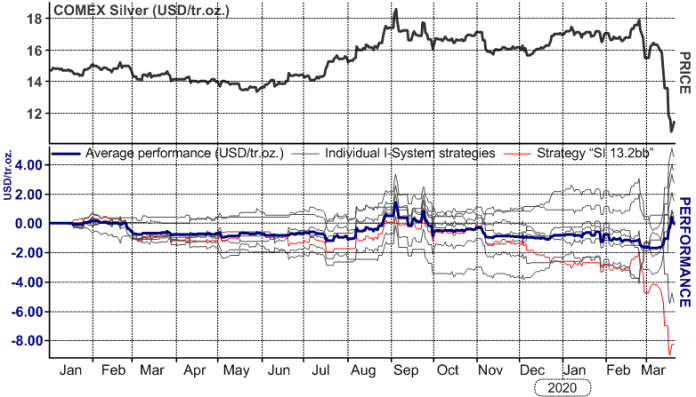

2. Silver

In some ways, trading was more interesting in COMEX Silver futures. There, an abortive trend through last summer generated some welcome gains, but as Silver relapsed into a side-ways drift between $17 and $18/tr.oz, I-System strategies continued getting whipsawed and lost ground. The price collapse in March reversed these losses, but its onset was so sudden that two out of the seven strategies sustained severe losses rather than gains. Nonetheless, the portfolio performed positively on average.

An important fact to note here is that I formulated these seven strategies more than ten years ago, in 2009. They have performed remarkably well over the years and I felt no urgency to refresh the portfolio’s ‘genetic code.’ That these legacy strategies behaved so well is a very important testimony to the quality of the I-System model.

Except for a short trending move through the summer of 2019, Silver has not been kind to trend following strategies. But the price collapse in March 2020 was ‘caught’ early and profitably by 5 out of 7 I-System strategies. However, one of the strategies – SI 13.2bb – stood out as an outlier, worth an expanded discussion.

While five of the strategies navigated the events very well, two of them sustained significant losses through the sharp price collapse this month. This merits an important discussion about the nature of trend following and some of its greatest challenges.

Fact of life: some strategies get killed…

The strategy that took the worst whipsawing over the recent months was SI 13.2bb. This underscores an important aspect of systematic trend following. Namely, even with well formulated trading strategies we still can’t escape uncertainty. While we can easily measure any strategy’s past performance, we have no way of knowing how it might do in the future.

After literally millions of performance simulations and nearly 20 years’ tracking and trading hundreds of I-System strategies, I can still not be certain which strategy will perform well in the future, and which one might fail. Any one strategy, regardless of how well it has performed in the past, could sustain substantial losses at any point in the future. This is just a fact of life. A screenshot of SI 13.bb is below:

COMEX Silver strategy SI 13.2bb had reached new performance peak in September 2019 (marked by square blue dot on performance chart) but sustained heavy losses as it navigated the subsequent trend reversals rather badly.

I-System’s ability to implement multiple strategies greatly improves the likelihood of achieving positive performance over time

This is precisely the reason we built the I-System so that it is capable of implementing a multitude of diverse strategies through the same knowledge framework. Using multiple strategies greatly enhances the odds of achieving positive performance over time and avoiding disappointments (as SI 13.2bb clearly would have been).

3. US 30-yr T-Bond futures

I reviewed I-System’s performance in US Treasury Bond futures over a longer time horizon, going back to 2016 to keep consistency with the review I published last September (“How we knew yields would collapse”) which also took January 2016 as its starting date.

Last year’s sustained up-trend staged a rather clean double-top reversal (I-System algorithms can identify double-top and head-and-shoulder reversal patterns) our strategies shifted to the short side and were briefly whipsawed in this year’s rally. However, they quickly reversed back to long again and reached a new performance peak this month, turning their initial risk budget of $25,000 into $52,563 at market close on Friday, 20 March 2020.

I-System also performed admirably well in other markets like the Nikkei, Russell 2000, S&P500, Copper, Silver and Gold. Over the coming deays I will endeavor to summarize some of them and also include Palladium where the ride has been most nauseating (but again well managed by our strategies).

For more information about the I-System and solutions we can propose for traders, asset managers and hedgers, please visit I-System Trend Following website.

Alex Krainer (xela.reniark@gmail.com) is a commodities trader and author based in Monaco. He wrote the book “Mastering Uncertainty in Commodities Trading.”