March 2020 market storm has been an important test of the I-System model and the way it navigated the unforeseen events. The results have been very encouraging and the system has done well in all affected markets. Last week I summarized its performance on Brent crude oil, Silver and US 30-year Bond. Here we take a look at how it performed in Russell 2000, S&P500 and Palladium markets.

1. Russell 2000

Russell 2000 peaked in 2018 and has traded mostly sideways ever since – not an ideal environment for systematic trend following. Its January 2020 peak at 1705 was followed by a slightly lower peak in February, and the subsequent price collapse triggered timely reversal signals. After bottoming about mid-way through Russell’s collapse, I-System strategies reversed their losses and gained 678 points.

Through the most recent price collapse on Russell 2000, I-System strategies generated strong gains by shorting the market. It is interesting to note the negative outlier strategy RL 10.1– it shows why we don’t haste to eliminate underperforming strategies. When the market crashed, RL 10.1 did better than all other strategies. The above results are net of transaction costs.

Why we hang onto underperforming strategies

Through February 2020, strategy RL 10.1 seemed like the worst one in the portfolio. But over the last 3 weeks, it was our top performer. This goes to show that we really can only know how a strategy performed in the past, but not how it would do in the future. At any time, your top performer might become your worst and vice versa. The best solution is to track a set of diverse strategies: some will do better, others less so, but the diversification gives us far better odds of achieving satisfying performance and avoiding disappointments in the future.

2. S&P500

The S&P500 was more challenging to trade than the Russell 2000. The key difference was that the Russell was not really in a bull market before crashing and its last peak in February was lower than its January peak. This is an important indication that the trend might be changing. By contrast, the S&P500 crashed more abruptly, from a strong bull market and new all-time highs. This is why I-System strategies signalled a reversal much sooner on Russell 2000 than on the S&P: they interpreted the decline as a correction at first and reversed to the short side only at 2,680 on average (20.87% below market peak). Even so, I-System performance on the S&P500 wasn’t without merit as it more than halved the S&P500 losses.

The March storm: S&P500 dropped -1,166 points; I-System only 578.

From peak-to-trough, the S&P500 declined 1,166 points (from 3,387 to 2,221). The worst peak-to-trough decline for the I-System strategies was less than half that: 578 points (from 232 to -346).

I-System strategies have reversed market losses through both big market corrections since 2018. If the current correction marked the beginning of an extended bear-market, I-System strategies will steadily gain over the S&P500 by trading the index on the short side. The above results are net of transaction costs.

If the current correction turns into an extended bear market, I-System strategies are very likely to significantly outperform long-only approach to investing, both on the S&P500, Russell 2000 and other stock market indices.

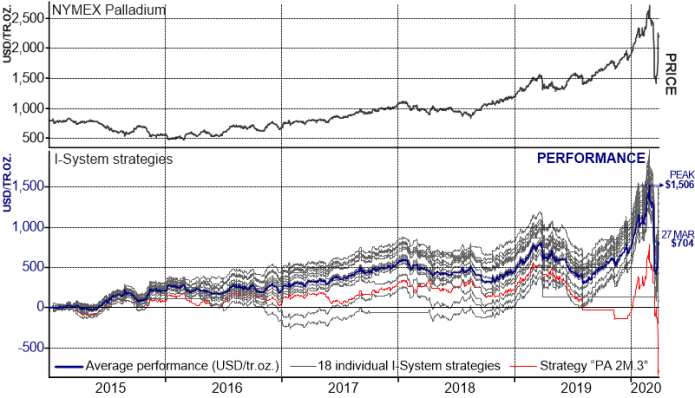

3. Palladium

Recent Palladium price fluctuations have been the most extreme we have ever experienced in any commodity market. Exhibit 3 looks at the trend that began in 2016 and suddenly came to a halt on February 27. Over the following 3 weeks Palladium price fell by almost 50%, from $2,712/tr.oz. to $1,420/tr.oz. – a completely unprecedented event.

Over the past five years I-System strategies generated gains both on the short side (2015) and the long side (2016-2020), making an average profit of just over $1,500/oz. However, the most recent price collapse significantly reduced that result in a very short order.

In spite of dizzying volatility, I-System performed well…

The price collapse happened suddenly and very rapidly. Four of the 18 I-System strategies reacted too late to profit from short exposure while 14 didn’t budge at all. In fact, by staying put, these 14 strategies actually performed well, given the circumstances.

I-System is not a mechanical trading system. There is a layer of judgment and interpretation in analysing market fluctuations. A price correction alone may trigger stop-loss and/or profit-taking signals, but it doesn’t easily trigger a trend reversal. Reversals typically involve double-top (or double bottom) formations, breaches of important trend-lines and a succession of peaks and troughs that diverge from prior trends. When a sufficient number of these elements are observed in a given market, a reversal decision may be triggered. Only then do we shift from trading long to trading short. Normally, this tends to work very well as it reduces the whip-sawing effect of periodic corrections and price consolidations.

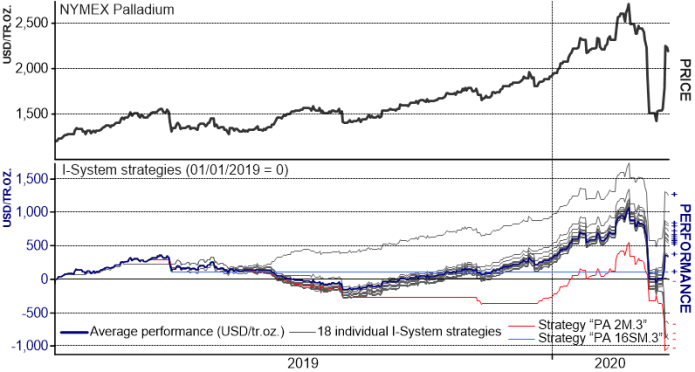

In this sense, there is a deliberate degree of inertia built into the ‘DNA’ of I-System strategies. While we can formulate strategies so that they are quicker to reverse from short to long and vice versa, our experience shows that strategies that trade longer-term trends tend to be most reliable performers over the long run. Consequently, the mix I prefer in any portfolio is about 2/3rds of strategies trading long-cycle trends with the remaining third being a mix of short-cycle and medium-cycle trends. This was true of the 18 Palladium strategies I put together for the “Altana Inflation Trends Fund.” The result was that the portfolio partly recovered its losses when Palladium price bounced sharply upward after its previous collapse. Exhibit 4 zooms in at the most recent 15 months of trading:

Looking at the last 15 months of trading, 13 strategies generated positive results (+) and only 5 of them sustained losses (–). The mix has been as expected: through a trending move, most strategies clustered around the average with always one or more outliers on either side. From a trend follower’s viewpoint, the big fail is strategy PA 16SM.3 which has not generated a buy signal in nearly 12 months. The above results are net of transaction costs.

The strategy I consider a failure is the one that fails to enter a position at all. A good example was strategy PA 16SM.3: for nearly 12 months it remained neutral as Palladium price soared by nearly $1,200/oz. This is the trend following equivalent of not casting your net as a large school of fish passed underneath your boat. Failure to capture value offered by market trends may be worse than acting and making mistakes. From a trend follower’s point of view, this is definitely worse and very annoying. This makes PA16SM.3 a prime candidate for elimination.

Regarding volatility and risk mitigation

The explosion of volatility in Palladium (and to a lesser extent most other commodity markets) was part of our objective reality – a fact of life, simply. It exemplifies the uncertainty we must inevitably contend with. When an event like this happens, we essentially have two choices: (1) to significantly reduce portfolio leverage or, (2) to not trade at all until the dust had settled and market environment returns to normal. Both of these are good choices in the short-term. Of course, there is also the choice of trading around the unfolding events to recover losses – but this fast track to ruin should be avoided at all cost.

Longer term, I believe that trading a judiciously diversified portfolio of financial and commodities futures with a well formulated, diverse set of trading strategies is better than ceasing trading altogether. As Thomas Aquinas pointed out, “if the highest aim of a captain was to preserve his ship, he would keep it in port forever.” People build ships not to preserve them, but to use them and generate positive economic value. This is true for any form of capital, particularly the kind that decays over time as predictably as cash does. Thus mitigating risk is advisable, but refraining from taking any risk is hardly an option.

Conclusion

Given the circumstances, I-System has passed the test of March market storm admirably well. I-System’s objective remains simply to meet uncertainty and capture value from market trends by implementing a set of well formulated trading strategies. I-System has reliably done this for nearly 20 years and again justified our confidence in it through entirely unprecedented events of the past few weeks.

This experience confirms yet again the model’s potential to transcend uncertainty by replacing it with a more predictable risk class – a swarm of undistracted, emotionless trading agents formulated within a stable, thoroughly tested knowledge framework that has proven valid for the purpose it was built for.

For more information about the I-System and solutions we can propose for traders, asset managers and hedgers, please visit I-System Trend Following website. •