Measured by historical standards, the price of oil has been extremely volatile in recent years. From over $114 per barrel in the summer of 2014 it collapsed more than 75% in only 18 months’ time. Then it tripled to $86/bbl in October 2018, only to drop by 40% to $52/bbl two months later. The question is, why is the oil price so very volatile? Is the market foreshadowing greater disruptions in the future? A closer look into oil supply and demand fundamentals suggests that a great crisis could be in the making – possibly with alarming repercussions.

The looming oil shortage

In 2012 a report produced by the UK Ministry of Defence predicted that oil prices would rise significantly out to 2040, and by “significantly,” they meant to $500 per barrel. From today’s perspective, this may seem farfetched. However, we should not dismiss UKMOD’s warning lightly. This could turn out to be the most important development facing humanity for decades to come.

Today, while demand for energy is growing by 1.5% per year[1], oil production is declining at a rate of between 4% and 9% per year, according to various industry sources. Even at the low end of these decline estimates, just keeping the oil production constant would require putting into production the equivalent of Saudi Arabia’s entire output every 3 years!

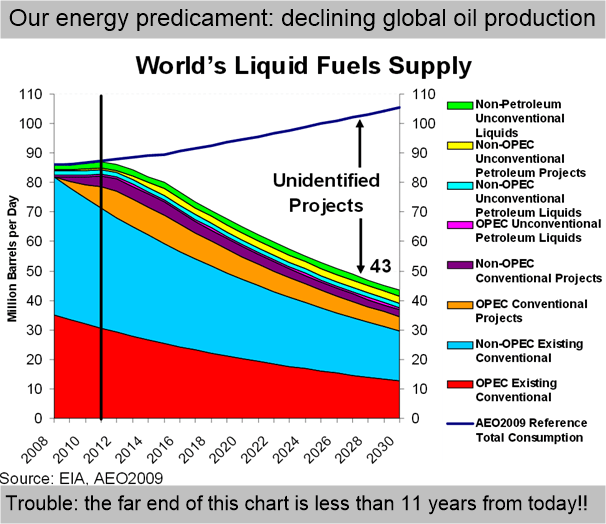

According to the U.S. Energy Information Administration (EIA), conventional oil production peaked between 2005 and 2009[2] with at least 37 oil producing countries already experiencing significant declines in production. A chart prepared by the EIA for a U.S. Department of Energy conference[3] in 2009 shows the agency’s projected global output decline through 2030 against projected demand:

Since 2009, the growth of shale oil production in the United States calmed the market’s concerns about oil supply. By today, it is clear that shale oil can’t bridge the supply gap. At best it has bought us some time.

The fading hopes of shale oil

Hydraulic fracturing of shale rock formations or “fracking” started to take off around 2005. Technology’s early success finally reversed the decline in American oil production, adding as much as 5 million barrels per day to U.S. output,[4] making U.S. world’s largest oil producer.

While fracking initially surpassed expectations, grounds for optimism have largely eroded as important limitations of the process became apparent. To begin with, early assessments of recoverable deposits were overly optimistic. Drilling experience further showed that shale oil wells deplete ten times faster than conventional wells[5] and that maintaining production requires enormous and ongoing capital expenditure to drill new wells. While early industry reports suggested that shale revolution would help push peak oil 40 years or more into the future, this assessment has turned out unwarranted.

In 2012, the International Energy Agency (IEA) estimated that U.S. production would keep growing beyond 2030. More recently, IEA conceded that U.S. shale oil production would peak around 2020[6]. Even the upbeat U.S. Energy Information Administration curbed their initial enthusiasm. In its 2014 World Energy Outlook, EIA warned that the U.S. shale boom in fact masked threats to world oil supply and that global energy system is in danger of falling short of expectations. This is a polite way of saying that we’re in serious trouble and fracking isn’t going to save us.

These concerns have been corroborated most recently in January 2019 when the Wall Street Journal published an analysis[7] showing that shale oil wells are falling well short of the industry’s expectations. After analysing 16,000 wells operated by 29 producers, it turned out that 66% of projections were “overly optimistic” by about 10% and some as much as 50%. According to Arthur Berman,[8] the most productive US shale basin, the Permian has only 7 years of proven reserves left. Berman was categorical that the reserves, “ain’t going to save the world,” and that “the growth is done!”

Clearly, shale oil won’t fill the 43-million-barrel-per-day gap marked in EIA chart as “unidentified projects.” Without very significant discoveries of new deposits, we’ll be facing a severe energy predicament in the near future. Oil won’t run out any time soon, but it is likely to get far more expensive.

The irreversibly diminishing returns on energy investment

The looming energy crisis seems more serious still when we analyze it in terms of the energy return on energy invested, or EROEI. International Energy Agency’s 2014 special report “World Energy Investment Outlook” asserts that meeting world’s energy needs will require investing $48 trillion through 2035. That sounds like a lot, but framing that investment in dollar terms is deceptive. Dollars can be “printed” in any amount as needed, but producing oil requires investment of real capital including materials, equipment and highly skilled labor. It also requires energy, and in many cases plenty of it.

In the 1930s and 1940s, oil producers obtained a return on invested energy of about 100:1 at the well-head. In other words, for the investment of 1 barrel of energy they obtained 100 barrels from the ground. This is what “cheap,” easily extractable oil was. By the 1990s, EROEI declined to about 40:1. Today, the world average is down to 15:1 and in the U.S. it is 11:1. Best shale oil basins yield an EROEI of 6:1 while deeper shale wells and tar sands yield 4:1 or less. Biofuels like ethanol from corn yield 1.5:1 or less.

Deterioration of EROEI economics has been accelerating. The energy we must expend to obtain new energy cannot be conjured up out of thin air. As more and more resources are required to generate the same amount of liquid fuels, energy production is becoming ever more expensive to society in real terms. And as it becomes more expensive in real terms, it must also become more expensive in nominal or dollar terms. That it has recently become cheaper in dollar terms can be only a temporary aberration.

Military and strategic viewpoint

I find it instructive to consult energy-related research by various military organizations as they are the one group that isn’t biased by an overriding financial stake in the energy markets. Over the years, I have come across three such reports – one by the German Army’s Bundeswehr Transformation Centre,[9] one by the U.S. Army Engineer Research and Development Center,[10] and one by UK’s Ministry of Defence.[11]

Each report considers the peak oil hypothesis with utmost seriousness and treats the notion that we have run out of cheap, easily extractable oil as a hard fact with grave consequences for the world economy, societies and global security. While U.S. Army report doesn’t mention “peak oil” as such, it is based on the notion that “The days of inexpensive, convenient, abundant energy sources are quickly drawing to a close… ” and discusses the likely consequences and contingencies for the U.S. Army.

German Army’s report affirms that the world is facing future oil scarcity. It notes that all of Germany’s key oil suppliers are past peak production and discusses the likely consequences in matter-of-fact but rather dismal terms. For example, the report sees peak oil as a global problem that could lead to breakdown of supply chains and global trade. High energy prices could disrupt financial markets, leading ultimately to a severe economic crisis, mass unemployment, infrastructure collapse, famine and a total system breakdown.

UK Ministry of Defence’s report is in agreement about peak oil, stating that “the imminent passing of the point of peak ‘easy oil’ will mean that hydrocarbon-based energy prices will rise significantly out to 2040.” MoD’s report projects that oil prices are likely to reach $500 per barrel. Consequences of the energy crunch might result in food shortages and a scramble for commodities and resources.

While this report was released in 2012, we have meanwhile seen further indications of the seriousness with which peak oil is regarded by the UK establishment. For example, UK Government’s Department of Energy and Climate Change (DECC), Bank of England and Ministry of Defence among others, have in secrecy conducted an ongoing peak oil workshop since at least 2009.

In 2010, The Observer has invoked the Freedom of Information Act to obtain the policy documents related to these workshops, but the DECC refused to release them, stating in a letter dated 31 July 2010 that these meetings are “ongoing” and “high profile” in nature. In 2015, none other than the Governor of the Bank of England, Mark Carney traveled to Riyadh to inquire about the future of oil and oil prices.[12]

Geopolitics: the significance of recent events in Venezuela

On 23 January 2019 Venezuela’s opposition leader Juan Guaido declared himself new president of Venezuela. The very same day, President Trump recognized Guaido as Venezuela’s legitimate leader. Less than a week later his National Security Advisor John Bolton spoke to Fox News stating that, “It will make a big difference to the United States economically if we could have American oil companies really invest in and produce oil capabilities in Venezuela.”

These dramatic developments and U.S. officials’ remarks seemed to dispense with the usual posturing around human rights and democracy bolstering. Explicit statements about the desire to develop Venezuela’s oil resources leave the impression that the issue has become too urgent to continue with the geopolitical business as usual.

More worrisome still was Treasury Secretary Steven Mnuchin’s 28 January statement that Venezuela can continue to export crude oil to the U.S. but that payments for those quantities would go to blocked accounts, inaccessible to Venezuela’s current government. This all but guarantees that oil flows from U.S. third largest supplier are likely ground to a halt if they can’t be taken by force. This crisis could now catalyze a veritable oil price shock in the near future.

Now what?

Shorter term opportunistic considerations for traders/hedgers: should traders rush out and buy crude oil futures or invest into oil company stock? Not necessarily and not immediately. The timing of large scale price events is unpredictable. They don’t start to unfold the day we become aware of the conditions that could trigger them. Furthermore, these events can start with an opposite price move, just as tsunami starts first with the ocean tide pulling out, before the sea comes rushing in.

Namely, oil price moves have been strongly correlated with US Dollar strength. Geopolitical crises often bolster the dollar exchange rate as investors rush to the perceived safety of the world’s reserve currency. In such a scenario, oil prices could resume falling – even sharply – before the conditions for the renewed rally ripen. Predicting and timing this sequence of events is impossible. A better approach is to ride the roller-coaster using systematic trend following strategies.

Observed day-to-day, markets appear to be driven by news events and data. However, extreme price events almost invariably unfold as trends that can span many months or even years, offering us ample opportunity to generate outsize profits. We achieve this by using systematic trend-following strategies.

Trend following has long and established track record for generating significant profits in commodity futures market. If you are not able to build a trend following model yourself (not necessarily an easy thing to do), you con subscribe to I-System / Altana Trend Compass daily reports. More about how that works is explained in the following 12-minute presentation:

Longer-term strategic considerations: for more than 100 years now, our societies have been built and organized as if we would always have abundant access to cheap energy. This might not hold true for much longer. Today, in terms of calories, about 50 times more economic output is produced by fuels than by labor. Inevitably we’ll have to adopt very significant readjustment to the way we produce, process and distribute food – just for starters. Much about that transition promises a bumpy ride, but in this respect my opinions and ideas are only as good as the next person’s – so this is a good juncture to wrap up this essay.

Notes:

[1] BP Statistical Review of World Energy estimates that between 2007 and 2017 world primary energy consumption has been growing at an average annual rate of 1.5%.

[2] In its 2010 edition of International Energy Outlook, U.S. Energy Information Administration (EIA) proclaimed that oil production from conventional sources probably peaked in 2006.

[3] “Meeting the World’s Demand for Liquid Fuels – A Roundtable Discussion” – U.S. EIA, April 7, 2009 – http://www.eia.doe.gov/conference/2009/session3/Sweetnam.pdf

[4] According to EIA, U.S. shale oil production attained 5.2 mb/d in December 2014

[5] According to a comprehensive analysis by David Hughes, oil geo-scientist and 30-year alumnus of the Geological Survey of Canada the average well output for the seven major shale basins declines from 60% to 91% during the first three years of production.

[6] “World Energy Investment Outlook” – OECD/International Energy Agency, June 2014 – http://www.iea.org/publications/freepublications/publication/WEIO2014.pdf

[7] Olson, Bradley et al. “Fracking’s Secret Problem – Oil Wells Aren’t Producing as Much as Forecast.” – Wall St. Journal, Jan 2, 2019.

[8] Arthur Berman is a geological consultant with 40 years’ experience in oil exploration, 20 years with Amoco (now BP). He published over 100 articles on geology and technology in oil exploration and more than twenty articles on shale oil production.

[9] Bundeswehr Transformation Centre – Future Analysis Branch: “Armed forces, capabilities and technologies in the 21st century: environmental dimensions of security” www.energybulletin.net/sites/default/files/Peak%20Oil_Study%20EN.pdf (112 pages).

[10] “Energy Trends and Their Implications for U.S. Army Installations” – U.S. Army Engineer Research and Development Center (ERDC), U.S. Army Corps of Engineers, September 2005 – unfortunately, this report is no longer available. An article about the report – “U.S. Army: Peak Oil and the Army’s Future” by Adam Fenderson is available at http://www.resilience.org/stories/2006-03-12/us-army-peak-oil-and-armys-future

[11] “Strategic Trends Programme: Regional Survey – South Asia out to 2040,” UK Ministry of Defence – Development, Concepts and Doctrine Centre (DCDC), October 2012. – DCDC is MoDs think tank within the Defence Academy site at Shrivenham. – The report utilised the input of a range of government agencies and departments, including the MoD’s Strategy Unit, the Defence Science and Technology Laboratory, the Cabinet Office, and the Foreign Office – as well as two private institutions, Standard Chartered Bank and Now & Next. Decc is notably missing from the list of contributors. A copy of the report is available here: https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/49954/20121129_dcdc_gst_regions_sasia.pdf

[12] Durden, Tyler. “What Saudi Arabia Told the Bank of England About Why Oil Crashed and Where it is Headed Next.” – ZeroHedge, 16 March 2015 – the article relates prepared remarks by Dr. Ibrahim Al-Muhanna, Advisor to the Minister of Petroleum and Mineral Resources of Saudi Arabia at the Institute of International Finance Spring Membership meeting.

[13] The forecasts were produced by Altos, DBAB (Deutsche Bank Alex Brown), EEA (Energy and Environmental Analysis), EIA (Energy Information Administration), IEA (International Energy Agency), GII (Global Insight, formed in Oct. 2003 through the merger of Data Resources Inc. and Wharton Econometric Forecasting Associates), NRCan (Natural Resources Canada), PEL (Petroleum Economics), and PIRA. Source: Energy Information Administration “International Energy Outlook 2003.”