Category Archives: Hedging

Six Principles To Adopting Best Practices In Commodity Price Hedging

- This week Sinopec disclosed the latest hedging mishap, losing $690 million amid last year’s oil price collapse.

- Unless price risk management is organized as an integral part of core business operations, it can devolve into eratic and risky game of speculation that can cause massive damage.

- The six simple but important guiding principles could help commodity firms create a world class risk management process and turn price risk into a source of value and competitive advantage.

This week Sinopec disclosed that it had incurred $690 million in losses in the fourth quarter of 2018. The losses were attributed to Unipec’s oil hedging bets. Unipec clearly took the wrong directional exposure to oil prices in the period when they staged a sharp, 40% collapse (October-December 2018). This much is understandable. However, such losses did not need to happen – I maintained heavy exposure to oil prices over the same period and not only avoided heavy losses but actually generated significant profits by simply adhering to a systematic trend-following model.

The coming oil price shock: could the crisis in Venezuela trigger an energy crisis?

Measured by historical standards, the price of oil has been extremely volatile in recent years. From over $114 per barrel in the summer of 2014 it collapsed more than 75% in only 18 months’ time. Then it tripled to $86/bbl in October 2018, only to drop by 40% to $52/bbl two months later. The question is, why is the oil price so very volatile? Is the market foreshadowing greater disruptions in the future? A closer look into oil supply and demand fundamentals suggests that a great crisis could be in the making – possibly with alarming repercussions.

The looming oil shortage

In 2012 a report produced by the UK Ministry of Defence predicted that oil prices would rise significantly out to 2040, and by “significantly,” they meant to $500 per barrel. From today’s perspective, this may seem farfetched. However, we should not dismiss UKMOD’s warning lightly. This could turn out to be the most important development facing humanity for decades to come. Continue reading

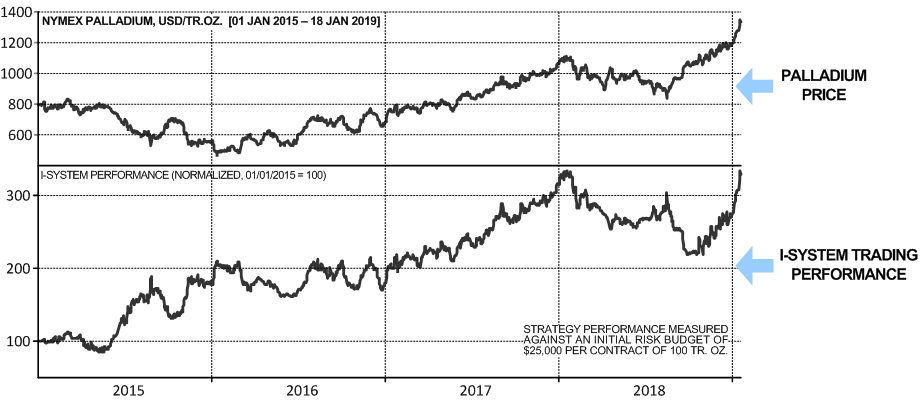

How trend following can help industry hedgers: the Palladium edition

Palladium price has more than doubled since the early 2016 making the white metal more valuable than gold for the first time since 2002. Its impressive performance attracted much attention from the financial press, which published numerous articles and analyses about the palladium market. If you diligently read the analyses, you may learn that automotive industry accounts for some 75% of demand for palladium, that its global production is as little as about 200 metric tons per year (vs. about 3,000 tons for gold), that only two countries (Russia and South Africa) produce more than three quarters of its global supply, and that the demand for palladium is expected to continue to grow. Presumably that implies that palladium price should remain high and possibly continue to rise. Continue reading

Groupthink in commodity price forecasting, its disastrous consequences and how to master price uncertainty

- In financial and commodity markets, large-scale price events are not predictable. Even so, most market professionals rely on forecasts most heavily in making forward-looking decisions.

- At times, this has disastrous consequences (see below)

- Large-scale price events are far and away the greatest source of external risk for commodity-related businesses. Their severity and frequency has been on the increase in recent years.

- An alternative approach to mastering uncertainty is to explore systematic trend-following strategies which, if used appropriately can turn price risk into a source of profit and hard to match competitive advantage

According to the latest Reuters survey, over one thousand energy market professionals expect the oil price to average between $65 and $70 a barrel in the years 2019 through 2023. Only 3% of respondents thought that Brent Crude Oil might increase above $90/bbl next year. So, market experts do not expect any surprises and largely agree that oil price will remain where it is. This groupthink reminds me of a similar situation some 15 years ago. Continue reading

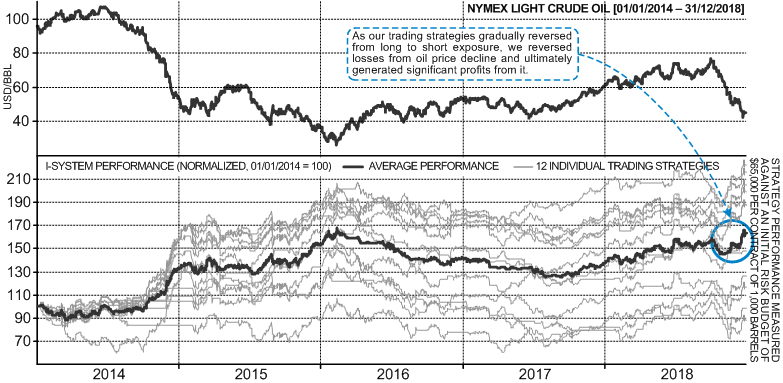

How we navigated the oil price roller coaster

Extreme price events are far and away the greatest source of external risk facing oil and gas producers and other energy-dependent companies. Frequency and severity of such events has been increasing dramatically since about 2005/2006 causing ocasionally severe pain for many industry participants.

Case in point was the 70% oil price collapse through 2014 and 2015, from over $100 to below $30 per barrel. In the aftermath of this decline, U.S. mining industry – which includes oil and gas producers – reported losses of $227 billion, wiping out eight previous years’ worth of profits as the following chart shows: Continue reading

Trading COMEX Copper with I-System technology

The price of Copper has been trending significantly higher since the start of 2016. However, this trend has not been easy to trade using traditional trend following strategies.

This last event (D) was quite painful for most – if not all – trend followers, as the following chart illustrates: Continue reading

Speculation in the natural world

Nature has … some sort of arithmetical-geometrical coordinate system, because nature has all kinds of models. What we experience of nature is in models, and all of nature’s models are so beautiful. – R. Buckminster Fuller

Nature’s survival strategies that bear the most similarities to activities of market speculators are those of predators. To live, predators must hunt and this activity includes elements of speculation. Like trading, predation requires knowledge, skills, judgment and decision-making. It also entails risk and uncertainty. A predator can’t be sure where her next meal is coming from. Each hunt is an investment of resources; it involves the risk of injury and loss of energy expended in failed hunts, which tend to be more frequent than successful ones. To survive and procreate, predators must consistently generate a positive return on this investment. Too much of a losing streak could turn out to be fatal. In his book, “The Serengeti Lion: A Study of Predator-Prey Relations” George B. Schaller painstakingly documented the details of hundreds of hunts by large cats in the Serengeti National Park in Tanzania. We have all seen wildlife television programs showing lions and cheetahs hunting, but Schaller’s work offers a much richer account of the life of predatory cats including their hunting behavior.

The anatomy of a hunt Continue reading

On effective trend following strategies

A question frequently arises among trend followers on the nature of effective trading strategies. The old school of thought holds that strategies should be simple, ultra robust and effective across markets and time frames. I happen to disagree so here I share a hard-won piece of knowledge that should help settle this question. Continue reading

Is an epic energy crunch in the making?

Last year I published a report with the (justifiably) bombastic title, “$500 per barrel: could oil price rise tenfold?” One of my central claims was that producing oil requires investment of real capital including materials, equipment and highly skilled labor, and that, “as more and more resources are required to generate the same amount of liquid fuels, energy production is becoming ever more expensive to society in real terms.” Thus, as it becomes more expensive in real terms (as the deteriorating EROEI figures indicate), the fact that energy has recently become cheaper in nominal (dollar) terms can only be a temporary abberation. EROEI stands for energy return on energy invested; in the early 1900s, we obtained 100 barrels euqivalent of oil per barrel invested (EROEI of 100 to 1); today we are at about 15 to 1 globally and at 11 to 1 in the USA. Continue reading