A question frequently arises among trend followers on the nature of effective trading strategies. The old school of thought holds that strategies should be simple, ultra robust and effective across markets and time frames. I happen to disagree so here I share a hard-won piece of knowledge that should help settle this question.

Life can only be understood backwards; it must be lived forwards – Søren Kierkegaard

Most trend followers use systematic trading strategies formulated on the basis of historical price data. For a quantitative approach to trading, we might expect to find a fairly strong consensus among its practitioners about what makes a good trading strategy, but that’s not the case. In addition to quantitative techniques, trend following entails a philosophical system of thought that shapes trend followers’ convictions. Beyond the fundamental idea that markets move in trends, philosophies and convictions vary considerably.

With regard to the question about what makes trading strategies effective, one school of thought among trend followers holds that strategies should be simple and ultra-robust: they should not only perform in most time-frames and trading environments, they should also perform well in any market. In other words, a strategy that’s successful in Soybean futures should also work on Gold, Natural Gas, and Yen futures. As a trend follower I find this idea surprising and happen to strongly disagree with it: each market manifests different price fluctuation dynamics and I find it hard to conceive that any one strategy can perform well in many different markets. What’s more, each market’s fluctuation dynamics may change over time, so we should expect some strategies to lose their edge. But then again, I’ve come across many trend followers who would vehemently disagree.

The reason why such questions remain contentious and why opinions about them still differ is because the issue is extremely difficult to settle scientifically. It would take a fairly long time forward-testing a set of trading strategies, periodically formulating new ones and running them in parallel along with the old ones to establish whether new trading strategies actually added value. Such strategies should also be qualitatively similar so that we can be sure that we are comparing apples with apples. This is in itself hard to achieve since there is much turnover among trend followers as older ones with their legacy models fail, quit, or simply retire and new ones enter the fray with new models.

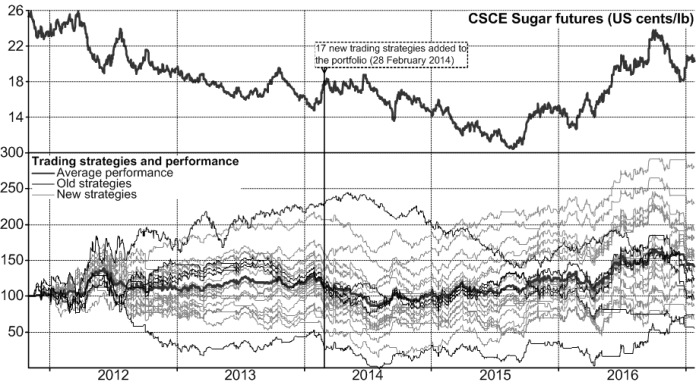

What we are about to explore might for this reason be a rather unique and hard-won piece of knowledge which might settle this issue. At Altana Wealth, our trend following strategies are based on a model I have developed and used continuously for over 13 years. “I-System” is a tool for generating strategies in different markets and over different time frames, but always within the same framework of knowledge. Even though strategies vary widely in the way they generate buy and sell decisions, these are always based on the same identical set of algorithms, so we can be sure here that we are comparing apples with apples. In the case below, the apples are strategies formulated for CSCE Sugar futures.

When we launched our inflation-hedge fund, we used five strategies to trade Sugar. These were formulated in 2006 and performed quite well over the years. In 2014, I decided to add 17 new strategies to the portfolio so that we could use 22 strategies to trade our 22 contracts position limit. I have implemented these in February 2014. A recent review of their performance revealed a striking difference between the old and the new strategies. The chart below shows the performance of the 22 strategies over the full period since AITF’s launch in November 2011.

As we can see, there’s significant variability in performance among strategies. The next chart lumps together the average performance of the five old strategies vs. the 17 new ones to underscore their difference:

New strategies visibly performed much better since they were implemented, in spite of the fact that their 2014 draw-down was considerably worse than that of the old strategies. This is not because our model improved (it has not) but because over the years, Sugar price fluctuation dynamics changed and the new strategies, formulated in late 2013 and early 2014 were a much better match to the new market environment than were the old ones, formulated in late 2006. The chart below illustrates how much these fluctuation dynamics have changed:

Between 1992 and 2005, Sugar futures fluctuated rather evenly, but after 2005, price changes became much more volatile with the average weekly change more than doubling from 0.26 ct/lb to 0.54 ct/lb! It is clear that strategies that were designed to perform in one environment couldn’t negotiate a different one equally well. We should thus not be surprised that new strategies, formulated in 2014 performed so much better.

Perhaps we can now lay to rest the idea that strategies can be ultra-robust and equally effective across markets and time frames. Change may be the only constant in life and to make our portfolios adaptable, we should constantly bring new varieties into the ‘genetic pool’ of our strategies, eliminating the ones that become obsolete. The change we may observe in markets is gradual and we can only ascertain it with hindsight. For this reason, the process of adaptation is slow, but it’s a process we must take into account. The first step in that direction is dispensing with the idea that we should ignore change and continue to use a rigid and unvarying range of responses in a changing world.

Alex Krainer is an author and hedge fund manager based in Monaco. Recently he has published the book “Mastering Uncertainty in Commodities Trading“.