Category Archives: Economics

The coming oil price shock: could the crisis in Venezuela trigger an energy crisis?

Measured by historical standards, the price of oil has been extremely volatile in recent years. From over $114 per barrel in the summer of 2014 it collapsed more than 75% in only 18 months’ time. Then it tripled to $86/bbl in October 2018, only to drop by 40% to $52/bbl two months later. The question is, why is the oil price so very volatile? Is the market foreshadowing greater disruptions in the future? A closer look into oil supply and demand fundamentals suggests that a great crisis could be in the making – possibly with alarming repercussions.

The looming oil shortage

In 2012 a report produced by the UK Ministry of Defence predicted that oil prices would rise significantly out to 2040, and by “significantly,” they meant to $500 per barrel. From today’s perspective, this may seem farfetched. However, we should not dismiss UKMOD’s warning lightly. This could turn out to be the most important development facing humanity for decades to come. Continue reading

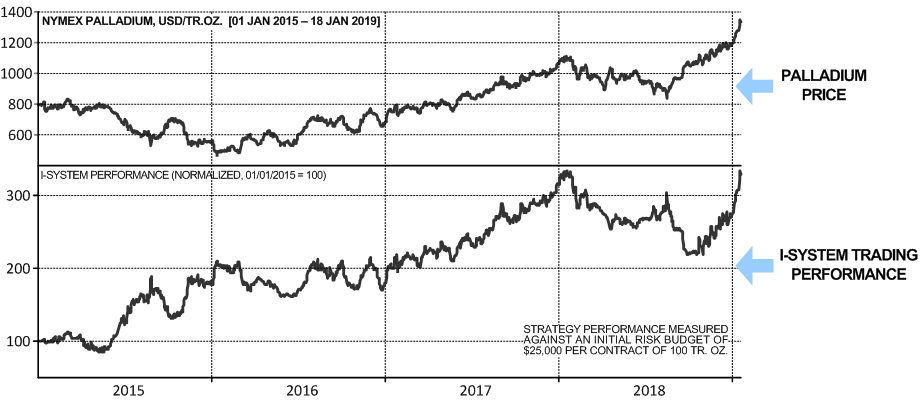

How trend following can help industry hedgers: the Palladium edition

Palladium price has more than doubled since the early 2016 making the white metal more valuable than gold for the first time since 2002. Its impressive performance attracted much attention from the financial press, which published numerous articles and analyses about the palladium market. If you diligently read the analyses, you may learn that automotive industry accounts for some 75% of demand for palladium, that its global production is as little as about 200 metric tons per year (vs. about 3,000 tons for gold), that only two countries (Russia and South Africa) produce more than three quarters of its global supply, and that the demand for palladium is expected to continue to grow. Presumably that implies that palladium price should remain high and possibly continue to rise. Continue reading

3/6: the strangulation of Russian economy in the 1990s was a deliberate IMF policy

… if the notion of billions of barrels of proven oil reserves and billions of tons of gold fills your dreams with visions of red-hot cash flow and ice-cold vodka, then Boris Yeltsin just might find some work for you. – Paul Hofheinz, Fortune Magazine, 23 September 1991[1]

The foregoing article is an excerpt from Chapter 3 of my book “Grand Deception: the Truth about Bill Browder, Magnitsky Act and Anti-Russian Sanctions.” Part 1 is here. Part 2 is here.

Shock therapy gave Russia one of the worst and longest economic depressions of the 20th century, an unprecedented humanitarian catastrophe for a peace time crisis, and a criminally inequitable privatization of public assets. The reasons why things happened this way in Russia generally aren’t well understood in the west. Even among better informed intellectuals, the failure of shock therapy is often thought to be vaguely related to some sinister flaw in the Russian society. It is what Bill Browder characterized as “the dirty dishonesty of Russia,” or “Russia’s evil foundation,” which spawned corruption and criminality of staggering proportions. In this toxic environment, the sweet fruits of western democracy and capitalism simply could not grow in spite of the generous benevolence of Russia’s western friends.

Continue reading1/6: How Russia decided to go from communism to capitalism in the 1990s

The foregoing article is an excerpt from the third chapter of my book, “Grand Deception,” which I wrote in response to Bill Browder’s bestseller, “Red Notice” but also as a retort to the relentless demonization campaign against Russia and its leadership in the West. Browder, an investor and hedge fund manager who made his fortune in the 1990s Russia, describes his fascinating experience during that time. However, he almost entirely glosses over the broader context within which events played out. Instead, he offers the same terse explanation he had regurgitated countless times in his various presentations and speeches, and it goes like this: after the collapse of the USSR, the government of Russia decided to go from communism to capitalism.[1] They thought that the best way to do this would be by giving everything away practically for free through various privatization schemes. Very rapidly, they transferred the nation’s economic resources into private hands.

But the unusual aspect of this transfer was that the private hands that received Russia’s wealth were not the same ones that had built it up since there were no restrictions on who could participate in the privatization program. As a result, the crown jewels of the nation’s productive resources ended up in the hands of a small group of oligarchs, most of whom covertly represented the interests of various western financiers.

Continue readingLabor tightness adds fuel to rising inflation in the U.S. economy

Toward the end of 2012, Elliott Management’s Paul Singer made a speech at the Archstone Partnership annual meeting. He stated that, “The thing that scares me the most is significant inflation, which could destroy our society.” About a year later in an interview with Wall Street Journal’s “Heard on the Street” program he explained that this could come about with small changes in perception of inflation risk: “The first whiffs of either commodity inflation or wage inflation … may cause a self-reinforcing set of market events … which may include a sharp fall in bond prices, … fall in stock prices, rapid increase in commodities…” Continue reading

Parabolic markets may signify onset of high inflation

Asset price inflation might signal debasement of the currency and acceleration of commodity price inflation

This time it may well be different… For several years now, numerous high-profile commentators and analysts have been forecasting an imminent stock market correction, or indeed a crash, evoking the events of 1929, 1987, 2000 or 2008. Of course, many are now predicting it is sure to happen in 2018. If not, perhaps in 2019 or maybe 2020? Who knows… But so far, not many analysts – if any, apart from yours truly – have considered the possibility that this rally might extend even higher from today’s dizzying heights. In an October 2016 post I suggested that this is exactly what was ahead. Continue reading

Deflationary gap and the West’s war addiction

In June of 2014, a group of American researchers published an article in the American Journal of Public Health, pointing out that, “Since the end of World War II, there have been 248 armed conflicts in 153 locations around the world. The United States launched 201 overseas military operations between the end of World War II and 2001, and since then, others, including Afghanistan and Iraq.” To be sure, each of these wars was duly explained and justified to the American public and for all those Americans who believe that their government would never deceive them, each war was defensible and fought for a good reason. Nonetheless, the fact that one nation initiated more than 80% of all wars in the last seventy years does require an explanation, which I submit below: Continue reading

Vladimir Putin’s 17 years in power: the scorecard

The following article summarizes many of the changes in Russia over 17 years under Vladimir Putin’s rule. All of the information presented is based on empirical data, most of it from western sources like the World Bank, Ernst&Young, Vtsiom, Ipsos and Gallup. Virtually none of this information was presented in any western corporate press with the notable exception of Forbes magazine (which took the information down after a few weeks). In addition to the below, I’ve subsequently published an article in three parts titled, “Is Vladimir Putin evil?“

Continue readingInflation: lessons from the last empire’s collapse

So far, the dreams of 1,000-year empires and stable world domination have eluded the ruling elites throughout history and across the globe. Empires arise, sustain themselves for a century or two and then rapidly decay and collapse. The collapse may appear relatively fast and obvious in hindsight, but in reality it spans decades, may appear as a series of temporary crises and only become obvious very late into the slow-motion train wreck. Continue reading