In April 2012, economist Robert Wenzel[1] was invited to speak at the Federal Reserve Bank of New York. On the occasion, he told the central bankers that “vast amounts of money printing are now required to keep your manipulated economy afloat. It will ultimately result in huge price inflation, or, if you stop printing, another massive economic crash will occur. There is no other way out.”[2]

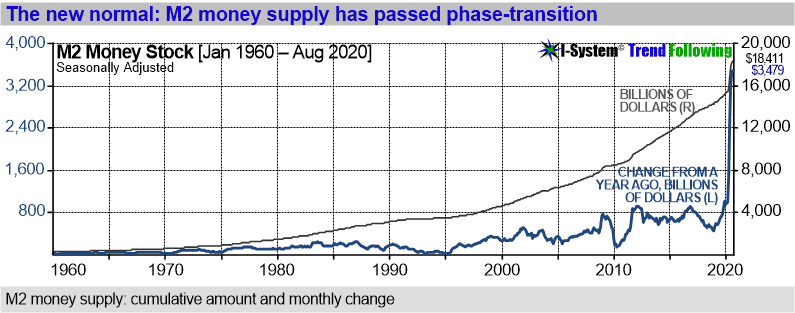

The money supply tsunami

Mr. Wenzel was right and after an attempted quantitative ‘tightening,’ and a 20% market crash in Q4 2018, the Fed capitulated and resumed money printing. That program has now sharply accelerated.

M2 money supply [3] is perhaps the most important early indicator of price inflation. In 2020, the Fed added almost $3.5 trillion to the aggregate. The transition is more striking still, in percentage terms:

Price inflation inertia

The relationship between money supply and price inflation is not linear; price inflation tends to move with some inertia. The 1970s inflation was preceded by the “Great Prosperity” of the 1960s: monetary expansion began in October ‘62 and continued through 1969. While money supply increased by 38% during that time, prices rose only 11% from April ‘62 to September ‘69. This inertia of price inflation convinced the era’s “New Economists” that inflation was a thing of the past. But inflation did emerge, only with a delay.

Velocity of money and human psychology

As new money enters circulation, there is a corresponding drop in money velocity since households don’t change their spending habits right away. They tend to use it to pay down debts and increase their savings so initially there is little upward pressure[4] on prices of goods and services. However, prices ultimately do catch up and when they begin to rise, velocity reverses course. From that point on price inflation begins to accelerate.

Gestation and the eruption of 1970s inflation

After seven years of growth fueled by deficit spending and credit expansion, U.S. economy began to overheat in 1969 and price inflation reached almost 5%. Nixon administration responded by instituting a tight money regime and extreme budget cutting. This led to a sharp recession.

A wave of mass layoffs and business bankruptcies spooked the government to abruptly reverse itself once more once more and increased deficit spending in the summer of 1970. Federal Reserve ramped up monetary inflation rate to 6.5% and the outlook quickly brightened again: interest rates plunged, stock markets soared and the nation was back on the high road to “prosperity.” But by now inflation began to accelerate and in 1974, it reached 11% and stayed high for the rest of the decade.

Destruction of wealth

Warren Buffett warned that for a debtor nation, inflation is the economic equivalent of the hydrogen bomb. It is the most formidable destroyer of wealth. Since 1960 over two thirds of the world’s market economies suffered episodes of inflation which exceeded 25% in at least one year.[2] On average, investors lost 53% of purchasing power during such episodes. In the U.S. between 1972 and 1982, price inflation averaged a “moderately high” 9% per year. It destroyed 65% of investors’ wealth in real terms.

What could trigger price inflation and when?

Although we can’t predict inflation’s timing or severity, history suggests that significant changes in inflation almost always come as a surprise. Ordinarily, three key factors act as economic flame retardants that absorb price inflation pressures:

- Asset price inflation: by initially absorbing most of the newly created money, financial assets deflect the pressure on prices of goods and services.

- Current account deficit has enabled the US to export its excess dollars to other nations (most notably China) and obtain cheap goods, keeping consumer prices low.

- Human psychology is slow to change inflation expectations, keeping money velocity low for a time.

Unforeseen changes in either of these elements could trigger a phase change in price inflation. Even a moderate increase in interest rates could burst the asset price bubble; economic protectionism and a breakdown in international trade could close the current account deficit, and a rise in commodity prices could boost inflation expectations and the money velocity.

Offshore dollars: another risk factor

Many people wonder why Japan, with its massive QE program hasn’t experienced any price inflation (yet)? The key difference between Japan and the U.S. is that the dollar is much more vulnerable to the actions of foreign creditors. While most of Japan’s debt is held domestically, foreigners hold more than $25 trillion in dollar denominated securities, short-term paper and offshore bank deposits. As Jens Parsson wrote in Dying of Money: “The economics of disaster commences when the holders of money wealth revolt. … Foreign holders of the money take fright … and their money elbows its way into the markets and reverses any balance of payments deficit.”

Will it be like the 1970s or could it be worse?

Economic imbalances that caused the 1970s inflation were mild compared to today’s conditions. Today, the trade balance, fiscal deficits, public and private debts, as well as money supply growth are much larger than they were in the 1960s. Even through the inflationary 1970s, the money supply growth remained below 14%. This year, we already blew past 23%. Predicting how these imbalances will play out is quite out of the question, but the risks are very serious and individuals as well as pension fund managers should consider taking bold action to protect their wealth from the ravages of inflation.

Solutions

For the 99% of us, gaining an effective hedge against the coming inflation tsunami will be difficult. Some investments are rather obvious: buying some silver and gold bullion. I don’t recommend you go overboard: have enough to cover a few months’ worth of your living expenses and to bribe corrupt government bureaucrats if necessary. Bitcoin might preserve some of your money’s purchasing power, but I remain cautious with regards to this alternative. I get the benefits of bitcoin but the risks of owning it tend to be understated by the enthusiasts. I’ll be a full convert only when my local grocer accepts bitcoin for a basket of groceries. Finally, owning a plot of farmland – even a small one – might be a good idea – for sure they can’t print more of that.

Ultimately however, we’ll have to act collectively. Our economies can function smoothly provided they have sufficient amounts of stable currency to serve as mediums of exchange. If currencies like the US dollar, euro and others are going to be debased, we can create local and regional currencies to keep the flow of goods and services going so people can exchange what they have to offer to the community and obtain what they need. This is not a radical idea: alternative currencies, including time banks have a long and honored history of lubricating local and regional economies so that the people may have access to the natural abundance that is our birthright.

For the 1%, the wealthier population segment, or managers of investment and pension funds, the options are rather different: for them, the most effective inflation hedge is a diversified commodity futures portfolio, (described at the link).

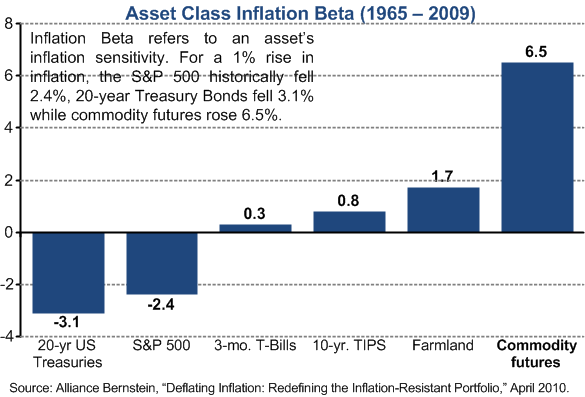

Commodity futures: the best way to protect your wealth

Empirical evidence shows that of all the asset classes, commodity futures provide the best inflation protection. Alliance Bernstein research found that “managed futures” (i.e. exposure to commodity futures prices) had the highest inflation beta of all asset classes:

A paper titled, “Assessing Managed Futures as an Inflation Hedge Within a Multi-Asset Framework,” published in the Journal of Wealth Management concluded that, “Managed futures outperform the other asset classes… No other asset class presents itself as a viable inflation hedge.”[6]

Indeed, as inflation erodes money’s purchasing power, commodity prices can rise very significantly. For example gold appreciated by 2,300% during the 1970s, from $35/tr.oz in 1971 to $850 in 1980. Inflation is likely to have a strong impact on other commodities as well, including energy, industrial metals and agricultural staples like wheat, soybeans, sugar, coffee, cotton and others.

Commodities: overdue for a major price readjustment?

In fact, a significant readjustment in commodity prices could be well overdue. Since the last financial crisis, the commodity prices have fallen to new historical lows relative to stock prices.

Just by reverting toward their historic norm, commodity prices could increase multi-fold. This process will likely unfold as a multi-year trend, offering perhaps a generational opportunity for investors to diversify their risk away from overinflated assets and gain a meaningful inflation protection at the same time.

Alex Krainer [xela.reniark@gmail.com] is a former hedge fund manager and author of the 5-star rated book “Mastering Uncertainty in Commodities Trading” and creator of I-System, probably the best trend following system ever built. Alex spent 8 years managing an inflation protection fund (2011 – 2019)

Notes:

[1] https://www.robertwenzel.com/

[2] Robert Wenzel, “My Speech Delivered at the New York Federal Reserve Bank.” Economic Policy Journal, 25 April 2012. http://www.economicpolicyjournal.com/2012/04/my-speech-delivered-at-new-york-federal.html

[3] M2 includes a broader set of financial assets held principally by households. M2 consists of M1 plus: (1) savings deposits; (2) small-denomination time deposits; and (3) balances in retail money market mutual funds (MMMFs). Seasonally adjusted M2 is computed by summing savings deposits, small-denomination time deposits, and retail MMMFs, each seasonally adjusted separately, and adding this result to seasonally adjusted M2. See https://fred.stlouisfed.org/series/M2SL

[4] By contrast, banks and corporations spend much of the new money to buy stocks and bonds or bolster reserves. This exerts upward pressure on financial asset prices.

[5] Stanley Fischer, “Modern Hyper- and High Inflations,” National Bureau of Economic Research Working Paper No. 8930