Investors exert a great deal of intellectual effort to determine the correct valuation of securities. Economic value is central to our decision making and it plays a major role in our intuitive psyche. In daily life, when we buy a loaf of bread or a tank of gasoline, we tend to have a good idea about what we think is cheap and what’s expensive. We like bargains, don’t enjoy being ripped off, and in the same way we’re inclined to shop for value as consumers, we find value investing intuitively appealing. But here’s the critical difference between buying goods and investing: shopping for investments is speculative while buying stuff isn’t, and speculation activates the part of our mental circuitry that can heat up to a boiling point and overwhelm any rational consideration of value.

On aggregate, speculative activity frequently produces price trends and in some cases bubbles. Here’s how this dynamic shapes up: in making investments, our rational goal is to obtain the best possible return with the least risk necessary. If we buy a house or a stock for investment, we want to receive a stream of rents or dividends and to have the opportunity to sell the asset for a price that’s higher than what we paid. Since those outcomes depend on other market participants, we are obliged to reflect on what they might do. Thus, if house prices are going up we infer that people are keen on investing in real estate and that rising demand would push future house prices even higher. If we are convinced that this is the case, we might disregard the fact that houses are already expensive. In effect, led by the actions of others, we might accept inflated house prices and proceed with the investment anyway.

This dynamic was demonstrated empirically in a clever experiment designed by Colin F. Camerer at Caltech’s Experimental Economics Laboratory [1]. In this experiment, a group of students were asked to trade shares in a hypothetical company during 15 five-minute periods. The students were not allowed to discuss their actions and only communicated via buy and sell orders. To start with, each student received two shares and some money with which to buy more shares. At the end of each of the 15 periods, the shares paid a $0.24 dividend for a total payout of $3.60 per share throughout the experiment ($0.24 x 15). This provision removed any uncertainty about the shares’ value: at the start of the experiment, the maximum value of one share was $3.60 and this amount diminished by $0.24 after each round, since that amount of dividend was already paid out. The highest price any player should accept to pay for a share should not be one penny more than what that share would yield in remaining dividends.

However, Camerer’s experiment showed otherwise. When the experiment started the share price immediately jumped to $3.50, close to the shares’ rational value. But rather than steadily declining with each new round, the price remained near that level almost to the very end of the experiment. Even when the value of each share fell below $1, students were still willing to pay $3.50 to buy them. When the experimenter asked the students why they bought the shares at prices that obviously far exceeded their value, the students would reply that, “Sure I knew that prices were way too high, but I saw other people buying and selling at high prices. I figured I could buy, collect a dividend or two, and then sell at the same price to some other idiot.”[2]

A strange confluence of circumstances produced this very same dynamic in a real-life experience that became known as the Chinese Warrant Bubble, described in a remarkable paper by Princeton University’s Wei Xiong and Columbia University’s Jialin Yu [3].

Chinese Warrant Bubble

In an effort to develop China’s financial derivatives market, from August 2005 the China Securities Regulatory Commission (CSRC) started introducing a small number of warrants – financial instruments similar to options, issued by publicly trading corporations. Firms were allowed to issue call or put warrants. With call warrants, issuing firms granted investors the right to buy stock from them, and put warrants gave them the right to sell stock back to the issuing company at a specified strike price and time period during which investors could exercise their option to buy or sell stock shares.

Between 2005 and 2008, 18 put warrants with maturities from 9 to 24 months were issued to the public. During this very period, Chinese stock market experienced a strong bull run and its index vaulted from 1,080 points in June 2005 to 6,124 in October 2007. This rally quickly pushed most put warrants so deep out of the money that they became worthless. In spite of this, feverish speculation on these securities produced an extraordinary financial bubble, unique in history of bubbles because warrants continued trading at spectacularly high levels of turnover and very inflated prices, even as it became evident that their value had clearly dropped to zero.

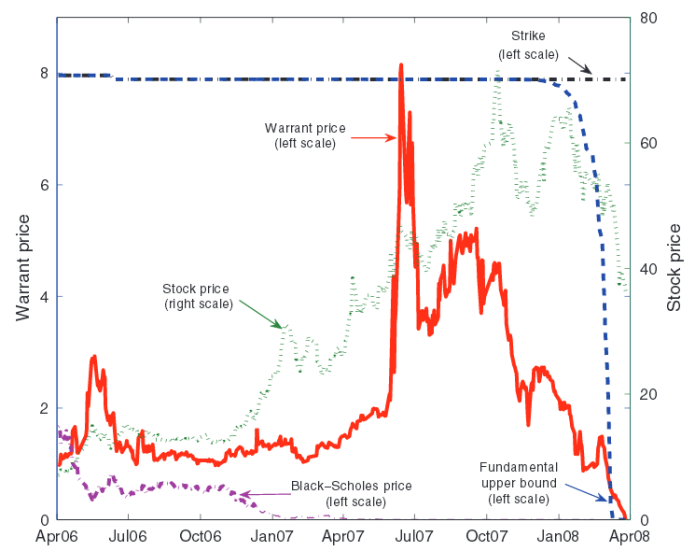

Consider the case of a Chinese liquor producer, WuLiangYe corporation. On April 3, 2006 WuLiang issued 313 million put warrants with a two year maturity and a strike price of 7.96 Yuan. The warrants’ initial price was 0.99 Yuan and company stock traded at 7.11 Yuan. Although the warrant was in the money when issued, the dramatic rise in WuLiang’s shares pushed it out of the money in only two weeks after which it never came back in the money. WuLiang’s stock price rose ten-fold, reaching 71.56 Yuan in October 2007 before retreating to about 26 Yuan on April 2, 2008 when the warrant expired. Rather than falling in value as it got farther out of the money, WuLiang’s put warrants rose along with the company’s shares, at one point even surpassing their own strike price at 8.15!

Price of WuLiang warrant. Note the astonishing gap between the market price (red line) vs. Black-Scholes valuation (purple). Source: The American Economic Review, October 2011.

Paying 8.15 Yuan (peak in the red curve in the above graph) for an instrument that had a maximum possible payout of 7.96 Yuan (if the firm’s share price went to zero) makes little sense, but someone did pay that much. Meanwhile, according to the widely used Black-Scholes model, the warrant’s value fell below 0.0005 Yuan after July 23, 2007 and remained below that level for the remaining nine months of the warrant’s maturity. Still, the warrant continued trading for several Yuan, dropping below 1 Yuan only in the very last few trading days, and dropping to zero literally in the last few minutes of the warrant’s last trading day.

This same phenomenon played out with all 16 put warrants analyzed by Wei Xiong and Jialin Yu. For each, Black-Scholes valuation dropped to zero (below 0.0005 Yuan) where it remained on average for 54 days. During this zero value period, each warrant traded at spectacularly high turnover levels [4] corresponding to billions of US Dollars per day and at an average price of 1.00 Yuan – more than 2,000 times their value.

Chinese warrants bubble provides the clearest evidence to date that in speculative decision making, our views about the actions of others can entirely override any rational appraisal of an asset’s value. That in turn gives us a convincing perspective on the reality of market trends: asset prices are not always driven by objective valuation only to be randomly affected by random external events. Instead, prices are driven by human psychology and its self-stoking collective action capable of sustaining major trends that can last many years.

As speculators we have little choice but to recognize trends as a real and legitimate source of investment opportunity. For investors, I believe this constitutes one of the most compelling reasons to use trend following strategies in their investment decision making. For more information and solutions please visit I-System Trend Following website.

The Chinese Warrants bubble case study was excerpted from my book, “Mastering Uncertainty in Commodities Trading.”

Alex Krainer has traded commodities since the mid-1990s. In 2016 he published the 5-star rated book, “Mastering Uncertainty in Commodities Trading.”

Notes:

[1] Surowiecki, James. The Wisdom of Crowds. New York: Anchor Books, 2004.

[2] Idem.

[3] Wei Xiong and Jialin Yu. “The Chinese Warrants Bubble.” National Bureau of Economic Research, Working Paper 15481 – http://www.nber.org/papers/w15481